Home

Applied Time Series Analysis

Loading Inventory...

Barnes and Noble

Applied Time Series Analysis

Current price: $112.95

Barnes and Noble

Applied Time Series Analysis

Current price: $112.95

Loading Inventory...

Size: OS

*Product Information may vary - to confirm product availability, pricing, and additional information please contact Barnes and Noble

Virtually any random process developing chronologically can be viewed as a time series. In economics, closing prices of stocks, the cost of money, the jobless rate, and retail sales are just a few examples of many. Developed from course notes and extensively classroom-tested,

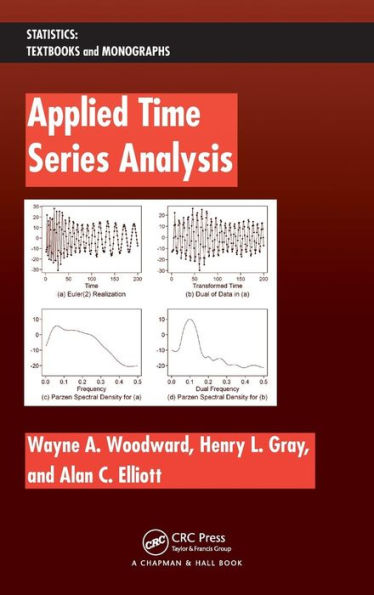

Applied Time Series Analysis

includes examples across a variety of fields, develops theory, and provides software to address time series problems in a broad spectrum of fields. The authors organize the information in such a format that graduate students in applied science, statistics, and economics can satisfactorily navigate their way through the book while maintaining mathematical rigor.

One of the unique features of

is the associated software, GW-WINKS, designed to help students easily generate realizations from models and explore the associated model and data characteristics. The text explores many important new methodologies that have developed in time series, such as ARCH and GARCH processes, time varying frequencies (TVF), wavelets, and more. Other programs (some written in R and some requiring S-plus) are available on an associated website for performing computations related to the material in the final four chapters.

Applied Time Series Analysis

includes examples across a variety of fields, develops theory, and provides software to address time series problems in a broad spectrum of fields. The authors organize the information in such a format that graduate students in applied science, statistics, and economics can satisfactorily navigate their way through the book while maintaining mathematical rigor.

One of the unique features of

is the associated software, GW-WINKS, designed to help students easily generate realizations from models and explore the associated model and data characteristics. The text explores many important new methodologies that have developed in time series, such as ARCH and GARCH processes, time varying frequencies (TVF), wavelets, and more. Other programs (some written in R and some requiring S-plus) are available on an associated website for performing computations related to the material in the final four chapters.